I found this sentence in Satyajit Das´s Blog - Fear & Loathing in Financial Products, and as the author says, an observation made by Goethe. It goes on:

On 30 July 1998, Alan Greenspan, then Chairman of the Federal Reserve argued that: “Regulation of derivatives transactions that are privately negotiated by professionals is unnecessary.” In October 2008, the now former Chairman grudgingly acknowledged that he was “partially” wrong to oppose regulation of credit default swaps (“CDS”). “Credit default swaps, I think, we have serious problems associated with them,” he admitted to a Congressional hearing. His current views on wider derivative regulation remain unknown. Politicians and regulators globally are currently busy drafting laws to regulate derivatives. A common theme underlying the activity is an absence of knowledge of the true operation of the industry and the matters that need to be addressed.

In DAVOS, at the yearly reunion for overrated Million- & Billionaires, surrounded by exactly those politicians, the common sense was that the economy is improving - and listening to Joe Ackermann from Deutsche Bank, one could think that the actual recovery is unstoppable. "Growth in emerging Markets remains strong", he says and as Greece gets downgraded to junk, he continues: "There is no way that Greece or Spain are going to default." Meanwhile, a solid framework for regulations on investment banking- and derivative transactions is not in sight. As the author Thomas Pynchon warned:

“If they can get you to ask the wrong questions then the answers don’t matter.” Simplistic causes and solutions may prevent real issues in relation to derivatives from being debated and dealt with."

The Obama Administration’s proposed “Volcker Rule” prohibiting major banks engaging in proprietary trading may, if implemented, affect speculative activity in derivatives. The proposal would prevent banks from hedging their own exposures using swaps as well as trading swaps. At a minimum, it would force banks to move their derivatives activities into non-bank entities. Transferring such activities would require additional capital (estimated at $20 billion or more) and also result in higher cost of funding for the derivatives activities. It is not clear how this proposal actually addresses any of the fundamental issues relating to derivative activities.

Hedging Activity?

The last week has ended with a sell-off that hit equity markets across the world. The main reason, market observer say, were the mounting tensions in Egypt. So is there fear in the market? Looking at hedging activity, the US CBOE Volatility Index Point & Figure chart is a helpful tool. The Index has made a quadruple bottom break down, a very strong sell signal but now the Index reverses this sell signal as it did a this very same level in spring 2010. So last week we have just seen a small reversal pattern that has not given buy signal yet. A break of the downtrend, indicated by the white line, would be a clear indication that equity markets are running into trouble and could head for a bigger downside move. But for now, it does not look as if investors are worried. In fact, the level indicates complacency.

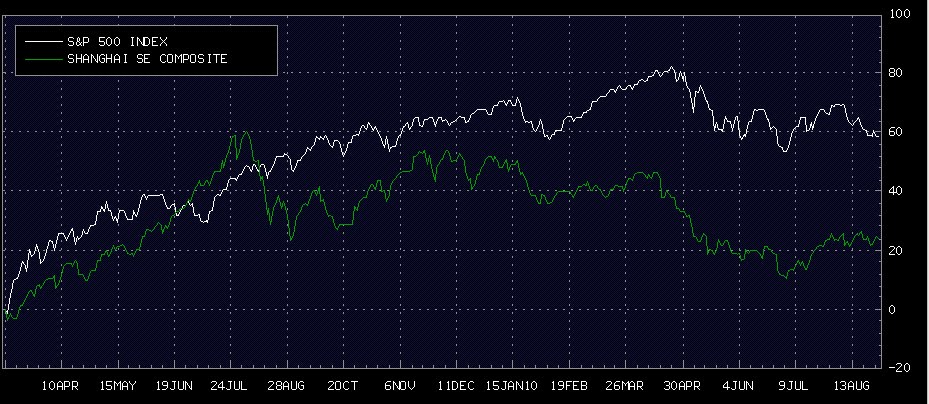

Focusing on the rally in commodities and equities that has started beginning of september 2010, we have to admit that some trends are broken and some could break soon. If markets are heading for a bigger correction can not be confirmed, nor ruled out at this point in time. I still view the biggest threat for financial market coming from the EUR and China, where as the US is certainly out of the woods for the next 6 month, probably the outperforming market until summer.

SPY 60´: Trend still up, but "break out profits" are gone.

QQQQ 60´: Trend break & a retest, starts to look topish.

{kind=link}